// now running · closed beta · for loan officers

The mortgage LOS with a brain.

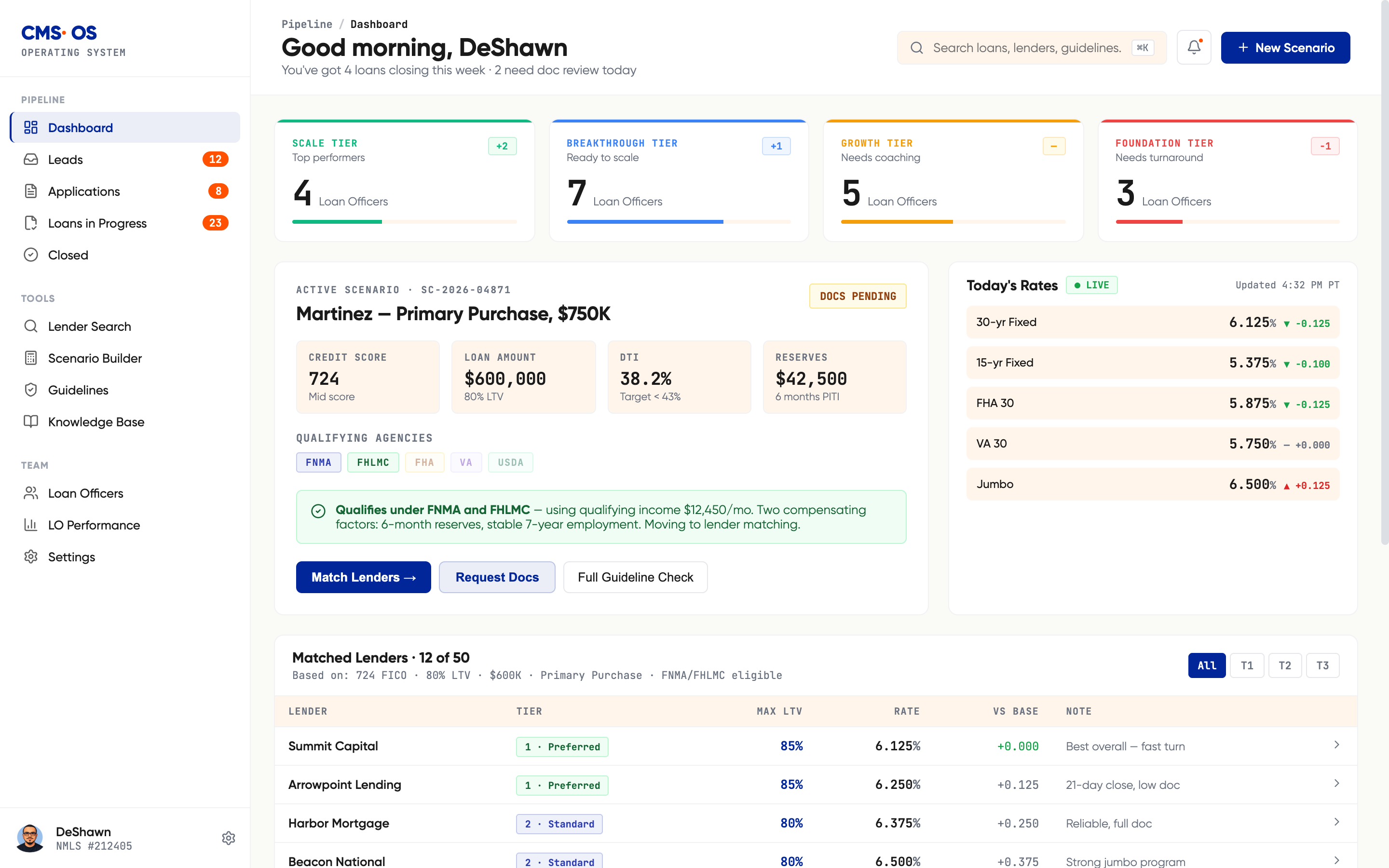

The stack your current shop won't build. 115 CMS loan officers close loans on it every day. If you want in, you have to be one of us — and cohort 02 is opening now.

½

the clicks per loan

30s

to a live scenario

1

tab, not six

🔒 app.cmsmortgage.com / pipeline

Open the live dashboard ↗